Debt collection is an essential part of any business entity. If you deal with fast moving consumer goods, then it’s likely that your customers pay for products immediately, whether it’s cash on delivery or ‘pay first, eat later.’ In such cases debt collection isn’t an issue because you always have your customer’s money (or card) in hand.

However, in many service-based businesses, the payment comes after your customer’s need has been met. This also applies to bulk industries where shipments are taken in large volumes that can’t feasibly be paid for in a single go. In situations where payment is made on a monthly or retainer basis, then collecting debts is a regular part of the business.

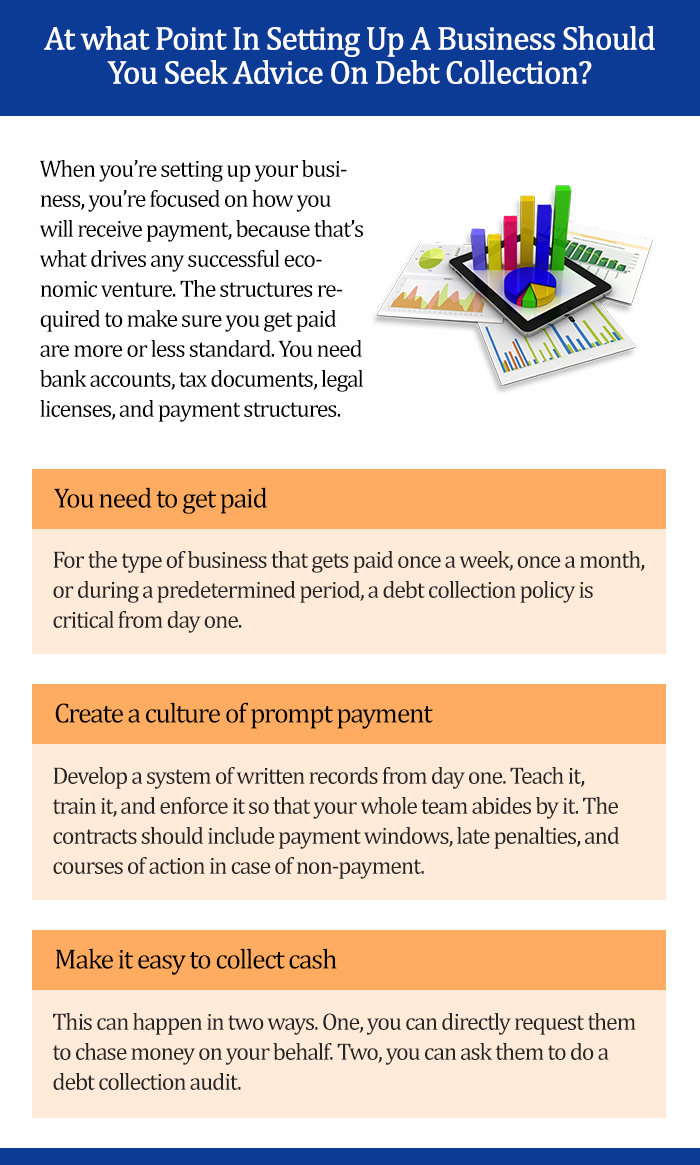

When you’re setting up your business, you’re focused on how you will receive payment, because that’s what drives any successful economic venture. The structures required to make sure you get paid are more or less standard. You need bank accounts, tax documents, legal licenses, and payment structures.

You need to get paid

On a micro level, you might require cash tills and electronic card readers. If your business is cash-heavy, you will need secure cash transit systems. This may involve an armoured service to bring cash to your premises at the start of each financial cycle or to deliver transacted money to the bank. Depending on business volumes, this can happen daily, or once a week.

For the type of business that gets paid once a week, once a month, or during a predetermined period, a debt collection policy is critical from day one. You don’t want to spend an entire month doing good work and then realise that you have no way of getting your client to pay you. As you’re laying the foundations of your business, think about its nature and structure.

The way you do business has a direct influence on your debt collection policy. While you’re drafting customer contracts and agreements, including clear payment terms, and put them in writing. While it may be tempting to use verbal agreements with your initial customers, it will set a dangerous precedent and is likely to give you problems later.

Create a culture of prompt payment

Develop a system of written records from day one. Teach it, train it, and enforce it so that your whole team abides by it. The contracts should include payment windows, late penalties, and courses of action in case of non-payment. You might feel this is a bit much in the first week of your business, but it could float or sink your company, so it does matter.

The next step is to write up an in-house debt collection policy. This task often falls to junior accountants, and they may not always have the clout to handle it. In an ideal world, people pay you when they say they will. In a more preferred situation, you ask someone for your money, and they pay it. In most cases, when you go looking for cash, people get defensive.

The average debt collection scenario is that a junior accountant goes to your client’s premises and gets shuffled between increasingly uncooperative staffers. In such cases, having a clear written debt collection guide will help your accountant deal with debtors.

Make it easy to collect cash

It can suggest a pattern they can follow, a script they can apply, and possibly even phrases and word choices they can use to get results. PR experts are good at this, and they can help you develop your debt collection training material. Consider this part of your start-up costs.

Fortunately, it’s never too late to get a debt collection consultant. At any stage in your business, you can hire an agency to follow up on your debts. This can happen in two ways. One, you can directly request them to chase money on your behalf. Two, you can ask them to do a debt collection audit.

As part of this service, the debt collection experts will review your business, its practices, its policies, and its debt volume. They can advise you on how to streamline your payment system, apply more efficient methods, and break the frustrating cycle of debt collection.

They can also analyse the nature of your business and advice you on whether it’s better to hire in-house debt collectors or get an external agency as a partner. Sometimes, it makes more sense to stick to your core business and let the cash collection experts handle theirs.

Related Articles: